Simple Trust Status on Form W-8BEN-E: What It Is and How to Fill It Out

When filling out Form W-8BEN-E, in Part I, Line 4, you face the choice of your organization's type. Among options like 'Corporation' or 'Partnership,' there are less common but important statuses, such as 'Simple Trust.'

What is this structure? Who is it for, and most importantly, how does choosing this status affect the rest of the form? Let's break it down.

What is a Simple Trust?

A Simple Trust is a specific type of trust that has three clear characteristics under U.S. tax law:

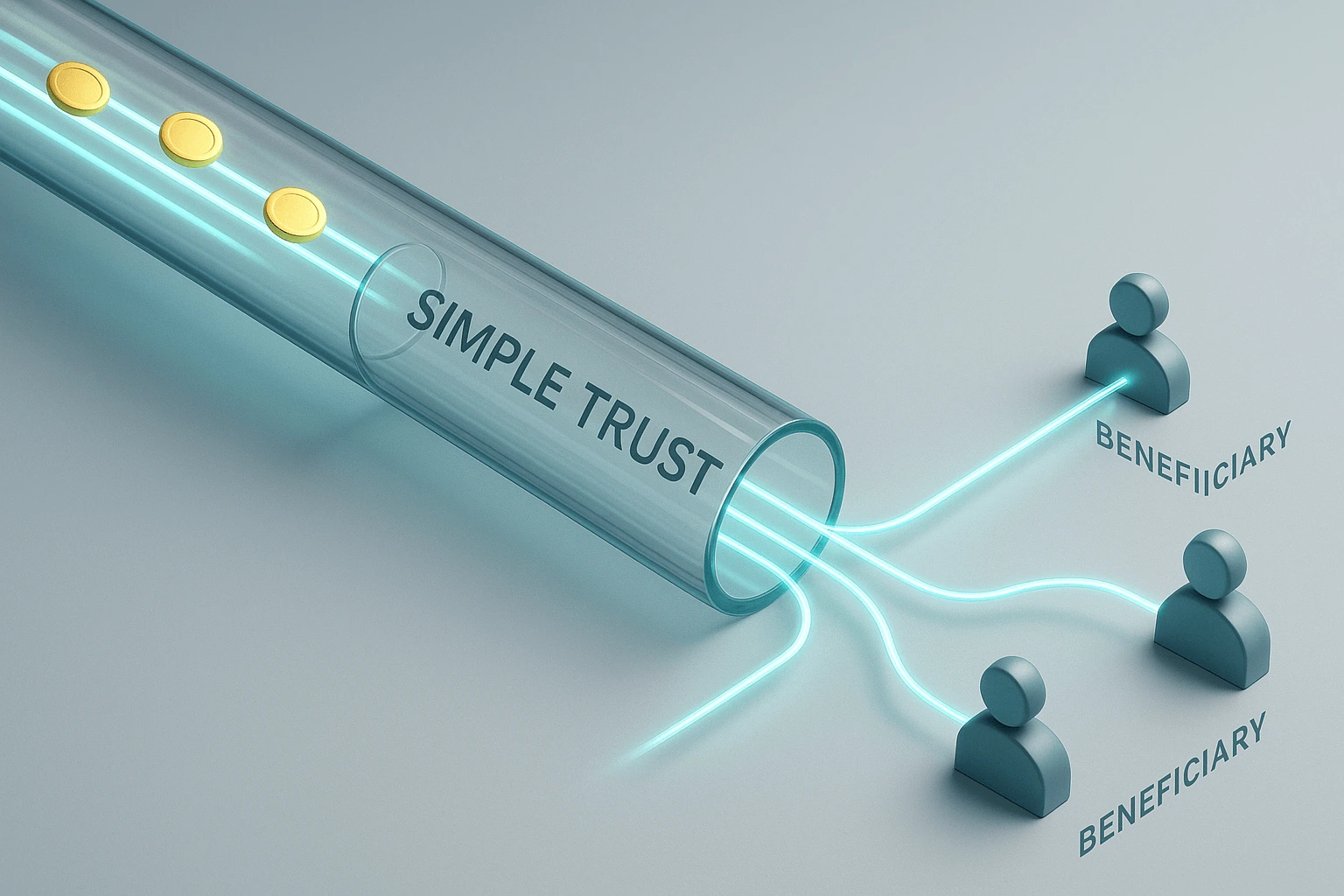

- Mandatory Income Distribution: A simple trust is required to distribute all of its income annually to the beneficiaries. It cannot accumulate profit.

- No Charitable Contributions: Such a trust cannot make donations to charitable causes.

- Distribution of Income Only: A simple trust only distributes the income earned in the current year, not the principal amount of the trust's assets (corpus).

Imagine a Simple Trust as a transparent financial channel. Everything that comes into it during the year must pass through it without remainder to the beneficiaries. If a trust has the right to accumulate income or make charitable contributions, it is considered a 'Complex Trust.'

When to Choose the Simple Trust Status on Form W-8BEN-E?

You should choose this status only if your organization is formally registered as a trust and its founding documents fully comply with all three criteria for a Simple Trust described above.

This is a legal classification.

Therefore, before selecting this status, we strongly recommend consulting with a lawyer or tax advisor who specializes in international law. An error in choosing the status can lead to incorrect taxation and complications.

Consequences of Choosing Simple Trust on the Form: What's Next?

If you have confidently chosen the 'Simple Trust' status in Line 4, this imposes a specific obligation on you in the next step.

The Hybrid Structure Question

Mandatory Answer in Line 5: The form requires organizations with 'Simple trust' status to answer the question in Part I, Line 5.

The question is: 'is the entity a hybrid making a treaty claim?'. A hybrid entity is one that one country (e.g., yours) treats as a separate legal entity, while another (the U.S.) treats it as a pass-through entity whose income is attributed to its owners. Completing Part III: If you answer 'Yes' to this question, you will need to complete Part III of the form — 'Claim of Tax Treaty Benefits'.

Conclusion

Choosing the 'Simple Trust' status is suitable for a narrow range of organizations and requires a clear understanding of its legal nature. The main thing to remember is that this trust does not accumulate income, and selecting this status on Form W-8BEN-E automatically leads to the need to analyze your organization's hybrid status and possibly fill out the tax treaty benefits section.

Not sure about your choice?

Our online builder with an AI assistant will guide you through these complex dependencies. Start filling out the form with us, and the system will automatically suggest the next steps you need to take.

Try our W-8BEN-E Generator